As an SEO expert who spends my days analyzing the algorithms that drive the web, I see a clear parallel between search rankings and home buying. In both worlds, “Authority” is everything. When you search for how much of a mortgage can i afford, you aren’t just looking for a random number; you are looking for your financial “Domain Authority”—the maximum limit of your buying power without risking a total system crash.

In April 2026, the housing market is operating on a new set of rules. Interest rates have stabilized at a four-week low of 6.30%, but inflation and property tax hikes in many regions have made the old math obsolete. To truly understand how much of a mortgage can i afford, you need to look at your income through the lens of a lender’s risk algorithm. This guide will break down the technical metrics, the hidden “metadata” of homeownership costs, and the human side of budgeting.

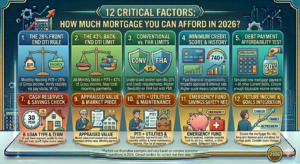

1. The “Keyword” of Affordability: The 28/36 Rule

The gold standard for any borrower asking how much of a mortgage can i afford is the 28/36 rule. Lenders use this to ensure you aren’t “house poor.”

-

The 28% Rule: Your monthly mortgage payment (Principal, Interest, Taxes, and Insurance—or PITI) should not exceed 28% of your gross monthly income.

-

The 36% Rule: Your total debt payments (mortgage plus car loans, credit cards, and student loans) should not exceed 36% of your gross monthly income.

2026 Affordability Benchmarks (Table)

2. Analyzing Today’s Market: April 2026 Rates

As of April 18, 2026, the average 30-year fixed mortgage rate is 6.34%. This is a significant drop from the 6.83% we saw a year ago, but it is still higher than the 6.09% low reached earlier this year. When you calculate how much of a mortgage can i afford, even a 0.5% shift in interest rates can change your purchasing power by tens of thousands of dollars.

For example, on a $400,000 loan:

-

At 6.34%, your monthly principal and interest is $2,486.

-

At 7.00%, that same loan jumps to $2,661.

That $175 difference might seem small, but over 30 years, it’s a $63,000 increase in the total cost of the house.

3. The DTI Algorithm: Conventional vs. FHA

Lenders “rank” your application based on your Debt-to-Income (DTI) ratio. If you are wondering how much of a mortgage can i afford with a lower credit score, an FHA loan might be your best bet, as they often allow a higher DTI than conventional loans.

-

Conventional Loans: Usually look for a DTI of 43% or lower, though some high-authority borrowers (those with 760+ credit scores) can stretch to 45%.

-

FHA Loans: Can go as high as 50% or even 57% in certain cases, though this is considered an “aggressive” financial position in the 2026 economy.

4. The Hidden “Metadata”: Taxes and Insurance

One of the biggest mistakes people make when asking how much of a mortgage can i afford is ignoring the non-loan costs. In 2026, property taxes vary wildly. For instance, the median annual property tax in New Jersey is over $9,300, while in Alabama, it is under $900.

If you buy a $400,000 home in a high-tax state, your property taxes could easily add $600 a month to your PITI. This directly reduces the amount of “Principal” you can afford to borrow.

5. Your Down Payment Authority

Your down payment is like the “backlink profile” of your loan application. The more cash you put down, the less risk the lender sees.

-

3.5% Down (FHA): High insurance costs (MIP), but lower entry barrier.

-

20% Down (Conventional): No Private Mortgage Insurance (PMI).

Removing PMI can save you $150 to $300 a month, which significantly boosts the answer to how much of a mortgage can i afford.

6. The “Human” Budget vs. The “Bank” Budget

Lenders care about your Gross Income (pre-tax). But you live your life on Net Income (take-home pay). As an SEO expert, I always recommend a “safe crawl” of your finances. If you have a $100,000 salary, the bank says you can afford $2,333 a month. But if you have high childcare costs or contribute 15% to your 401(k), that $2,333 might feel like a “manual penalty” on your lifestyle.

Always ask how much of a mortgage can i afford based on your after-tax reality, not just the bank’s maximum limit.

7. Maintenance and the “1% Rule”

A house is a physical asset that requires “content updates” (repairs). You should set aside 1% of the home’s value annually for maintenance. If you buy a $500,000 home, that’s $5,000 a year, or $416 a month. When calculating how much of a mortgage can i afford, make sure you have room for a new roof or a water heater.

8. Credit Score: Your Financial DA (Domain Authority)

In 2026, your credit score is the primary ranking factor for your interest rate.

-

760+ Score: You get the “Featured Snippet” rates (6.34% or lower).

-

640 Score: You might be stuck with 7.10%.

On a $300,000 house, that credit score difference can change the answer to how much of a mortgage can i afford by over $150 per month.

9. Calculating Affordability by Monthly Payment (Table)

If you have a specific monthly budget in mind, here is what that translates to in terms of loan amount (assuming a 6.34% interest rate, taxes, and insurance).

*Estimates include estimated 1.2% property tax and $1,200 annual insurance.

10. The Impact of Other Debts

If you have a $500 car payment, your “Borrowing Authority” drops instantly. In the lender’s eyes, that $500 could have covered roughly $80,000 in mortgage debt. Before asking how much of a mortgage can i afford, consider paying off high-interest credit cards or small personal loans to “optimize” your DTI.

11. Closing Costs: The “hidden fees”

Don’t forget the upfront costs. In 2026, closing costs typically range from 2% to 5% of the loan amount. For a $300,000 mortgage, you need $6,000 to $15,000 in cash in addition to your down payment. If you don’t have this, it directly affects the answer to how much of a mortgage can i afford.

12. Future-Proofing: ARM vs. Fixed Rate

With rates at 6.34%, some 2026 buyers are looking at Adjustable Rate Mortgages (ARMs). A 5/1 ARM might offer a rate of 5.68%. This allows you to afford a larger mortgage now, but it carries the risk of a “re-indexing” (rate hike) in five years. Only choose this if you plan to sell or refinance before the adjustment period.

Frequently Asked Questions (FAQs)

How much of a mortgage can i afford on a $75k salary?

Assuming you have no other major debts, the 28% rule suggests a monthly payment of $1,750. In April 2026, with a 10% down payment, you could likely afford a home priced around $260,000 to $280,000.

Does a car loan really affect my mortgage limit?

Yes, significantly. Every $100 in monthly debt can reduce your potential mortgage loan amount by approximately $12,000 to $15,000.

What is a “safe” DTI ratio for 2026?

While lenders allow up to 43%, a “safe” DTI is 36% or lower. This leaves you with enough “crawl space” in your budget for emergencies and savings.

How much of a mortgage can i afford with a 20% down payment?

A 20% down payment removes PMI and lowers your loan-to-value ratio. This usually allows you to afford a house that is 15-20% more expensive than someone with the same income but only a 3.5% down payment.

Why do property taxes matter for my mortgage approval?

Lenders don’t just look at the loan; they look at the total “Escrow.” If taxes are high, the bank reduces your “Principal” allowance to ensure your total monthly payment stays within their DTI limits.

Can I get a mortgage if I’m self-employed in 2026?

Yes, but you’ll need “high-quality content” for your application—typically two years of tax returns showing stable or increasing net income.

Conclusion

Determining how much of a mortgage can i afford is the most important “keyword research” you will ever do for your life. In the 2026 market, success isn’t about getting the biggest loan possible; it’s about “ranking” for a home that fits your life without draining your bank account.

By following the 28/36 rule, optimizing your credit score, and accounting for the “hidden metadata” like taxes and maintenance, you can step into the housing market with confidence. Remember, the goal is to “convert” a house into a home, and that only happens when you are financially comfortable.

Ready to see your real numbers? Pull your credit report, organize your W-2s, and start your 2026 home-buying journey with the precision of an expert. Now that you know how much of a mortgage can i afford, the only thing left to do is find the right property.

Disclaimer: This guide is for educational purposes. Mortgage rates and eligibility are subject to change based on individual financial profiles and market conditions. Consult a licensed mortgage professional for personalized advice.